UNIFIED VOLUNTARY ACCUMULATIVE SYSTEM "KELESHEK" AND ITS IMPLEMENTATION

16.11.2024 18:59:31 1544

UNIFIED VOLUNTARY ACCUMULATIVE SYSTEM "KELESHEK" AND ITS IMPLEMENTATION

In pursuance of the instruction of the Head of State dated September 1, 2023, announced in the address to the people of Kazakhstan "The Economic Course of a Just Kazakhstan", a unified voluntary accumulative system "Keleshek" (hereinafter – Keleshek) has been developed.

The main model of Keleshek will be implemented within the framework of the current site of the State Educational Accumulative System (GONS). Since 2013, more than 77 thousand bank deposits and insurance contracts have been opened.

In order to increase the attractiveness of Keleshek, it is planned to establish a starting educational capital from the state for children who turned 5 years old in the current calendar year 60 MCI (221,520 tenge) and 120 MCI for orphans (443,040 tenge), an annual payment of a state premium of 5% for all children, 7% for children from SUSN.

Keleshek also provides for the participation of parents in building the trajectory of children's education and thereby forms a culture of money savings for them.

Keleshek accounts can be opened in second-tier banks and insurance companies that are participants in child insurance. Currently, active partners in the field of GONS are: Otbasy Bank, Halyk Bank, Jusan Vapk, Nurbank and VTB Bank. In addition, Bank RBK, Eurasian Bank, Bereke Bank and the National Postal Operator Kazpost will also work with the introduction of Keleshek. In addition, cooperation with 5 insurance companies is carried out within the framework of the GONS. Cooperation is carried out only with existing stable financial institutions.

In this regard, parents, after opening these accounts, must annually make a minimum contribution of 12 MCI for children with disabilities and 24 MCI for other children.

The minimum amount of remuneration for banks is established on a legislative basis. So, not less than 200 basis points ( - 2%) for deposits concluded for up to 1 year inclusive (for example, if the base rate of the National Bank is 15%, then the annual effective rate should be at least 13%), not less than 300 basis points ( - 3%) for deposits concluded for more than a year (for example, if the base rate is 15% of the National Bank, then the annual effective rate should be at least 12%). At the same time, the money on these deposits is insured by the Kazakhstan Deposit Guarantee Fund, and the amount of insurance payments is insured by the Insurance Benefit Guarantee Fund.

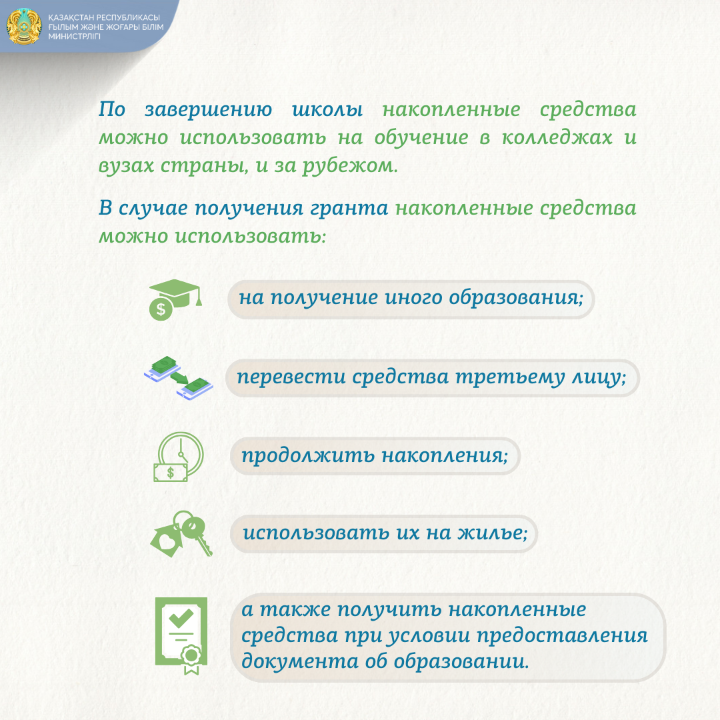

Upon completion of school, the accumulated funds can be used to study at colleges and universities in the country and abroad. In case of receiving a grant, the accumulated funds can be used to obtain another education, transfer funds to a third party, continue accumulating, use them for housing, and also receive the accumulated funds provided that a document on education is provided.

Thus, the funds accumulated by parents, taking into account the initial educational capital from the state, the annual state premium, investment income (remuneration from banks), as well as savings generated within the framework of the National Fund for Children project, will provide an opportunity to receive high–quality education or improve living conditions.

In this regard, after reaching the target purpose – to receive an education (a diploma of technical education or higher education), the depositor can use the additional right to transfer the accumulated funds to improve housing conditions by analogy with the National Fund for Children project.

Source : https://www.gov.kz/memleket/entities/sci/press/news/details/884074