Tax arrears: a differentiated approach to recovery

11.09.2025 12:00:17 4827

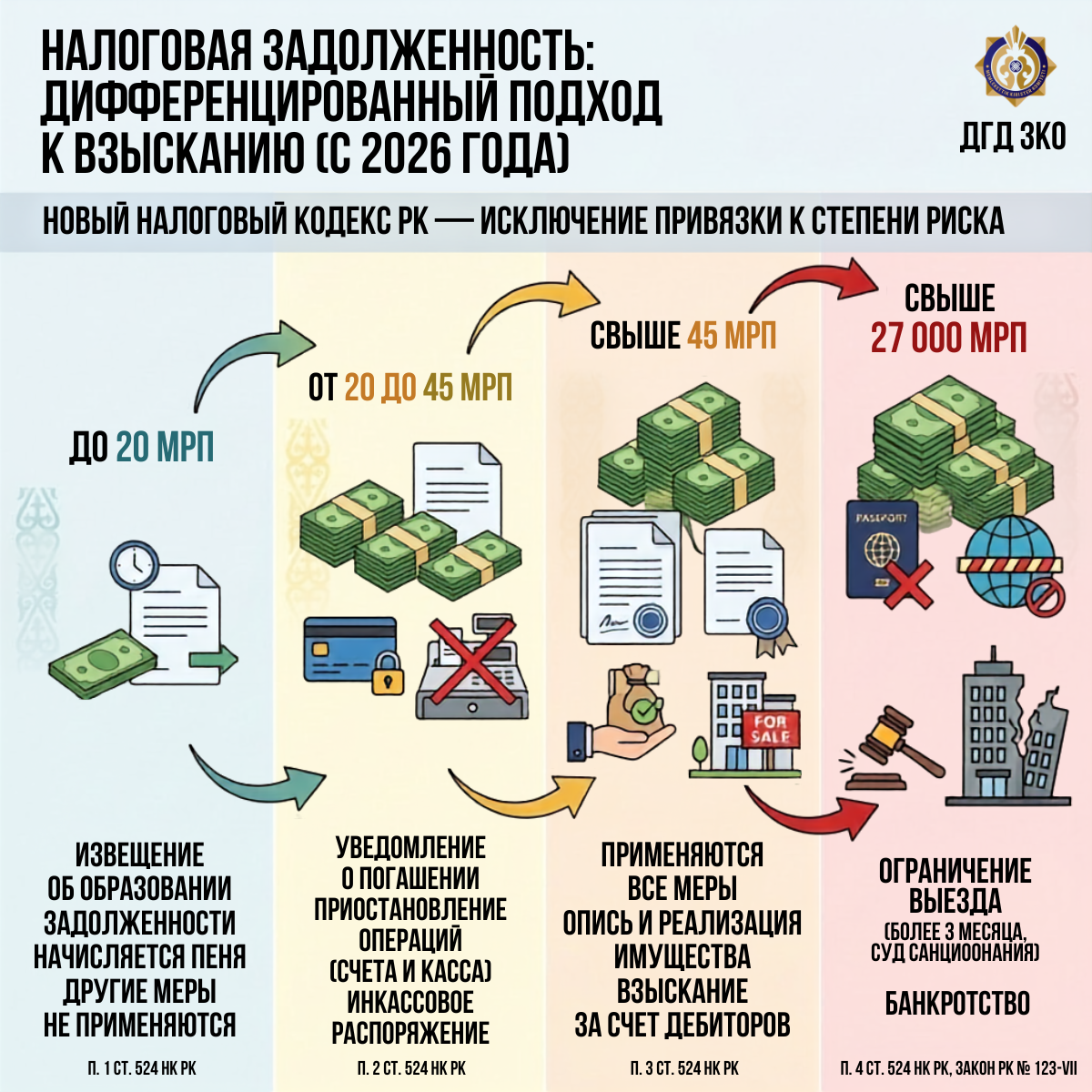

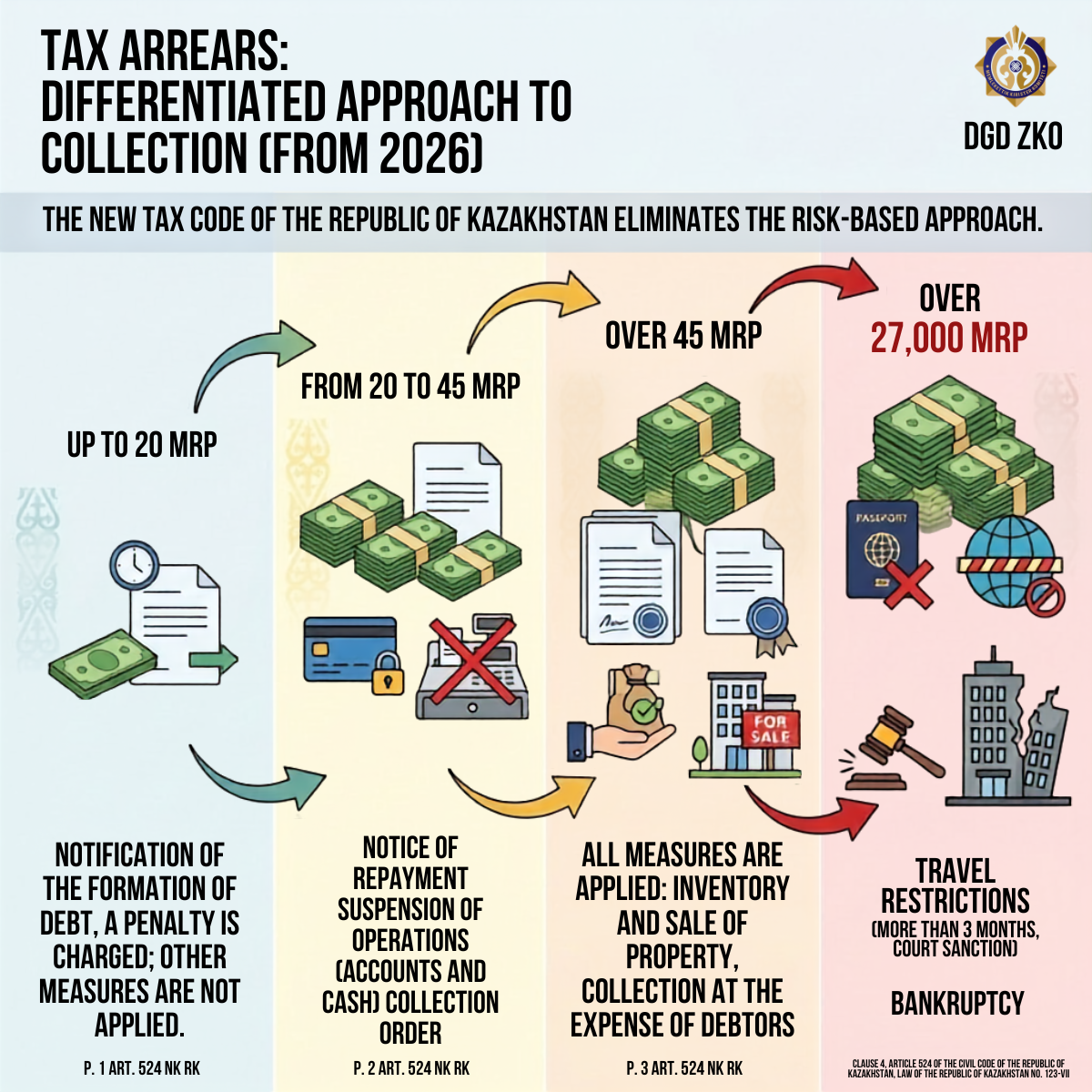

The new Tax Code of the Republic of Kazakhstan provides for a differentiated approach in the application of methods and measures for the compulsory collection of tax debts, with the exception of the link to the degree of risk. So, if now enforcement measures are applied in the amount of 1 tenge and above, taking into account the results of the RMS, with the exception of the suspension of spending operations on bank accounts, where an encumbrance is imposed on accounts with tax arrears exceeding 6 MCI, then from 2026 with tax arrears:

- up to 20 MCI - a notice of tax arrears is sent and a penalty is charged, no other measures are applied;

- from 20 to 45 MCI - a notification of repayment of tax arrears is sent, spending operations on bank accounts and cash registers are suspended, and a collection order is issued;

- over 45 MCI - all measures are applied, including inventory and sale of property, collection at the expense of debtors;

- over 27,000 MCI - the taxpayer's departure is limited (in case of non-repayment within 3 months based on court approval), bankruptcy.

Source : https://www.gov.kz/memleket/entities/kgd-zko/press/news/details/1246638?lang=ru