Analytical report on the results of an internal analysis of corruption risks in the activities of the Department of State Revenue in Astana

30.06.2026 18:36:29 8

In order to identify and study possible causes and conditions conducive to the commission of corruption offenses in accordance with the Constitution of the Republic of Kazakhstan, the Law "On Combating Corruption", the Model Rules for Conducting Internal Analysis of Corruption Risks, approved by Order No. 21 of the Chairman of the Anti–Corruption Agency of the Republic of Kazakhstan dated January 16, 2023 (hereinafter referred to as the Model Rules), dated March 27, 2026 No. 515 "On Conducting an Internal Analysis of Corruption Risks in the Activities of the State Revenue Department in Moscow Astana", as well as within the framework of the implementation of the standard basic direction No. 4 "Prevention and Combating Corruption" (hereinafter referred to as TBN No. 4), an internal analysis of corruption risks in the activities of the Department of State Revenue in Astana was conducted.

The internal analysis of corruption risks was conducted by a working group defined by Order No. 515 dated March 27, 2026, consisting of employees with practical experience in applying industry legislation in their activities: the deputy head, heads of Departments of the Department and customs posts.

Information system data and other analytical information have been studied to identify corruption risks and develop recommendations.

The internal analysis of corruption risks in the Departments and Customs posts of the Department was carried out in accordance with the Standard Rules and Instructions for the implementation of TBN projects No. 4 in the following stages:

1) collection and synthesis of information about the object of analysis;

2) analysis of legal acts and internal documents regulating the activities of the object of analysis, its organizational and managerial activities for the presence of corruption risks;

3)preparation and signing of the analytical report;

4) identification of positions subject to corruption risks;

5) control and monitoring of the implementation of recommendations to eliminate the causes and conditions conducive to the commission of corruption offenses identified by the results of an internal analysis of corruption risks.

In the course of the work, the following were analyzed:

- legal acts and internal documents regulating the Department's activities;

- provision of public services;

- appeals of individuals and legal entities in relation to the object of analysis;

- disbursement and allocation of budgetary and financial resources for the period of 2025 and the expired period of 2026;

- development and operation of information systems;

- establishing the facts of hiring persons who have previously committed a corruption offense;

- identification of persons engaged in activities incompatible with the performance of government functions;

- establishing the facts of the exercise of official duties in the presence of a conflict of interests;

- establishing the facts of the use of official and other information that is not subject to official dissemination in order to obtain or extract property and non-property benefits and advantages;

- sending civil servants to anti-corruption training.

Given the multiplicity of functions and the intersectoral nature of the Department's work, the main areas of activity were analyzed, namely:

1. development and operation of information systems.

According to the results of the analysis, 1 corruption risk was identified:

The area of activity covered by the analysis

1. Development and operation of information systems

1) The name of the corruption risk

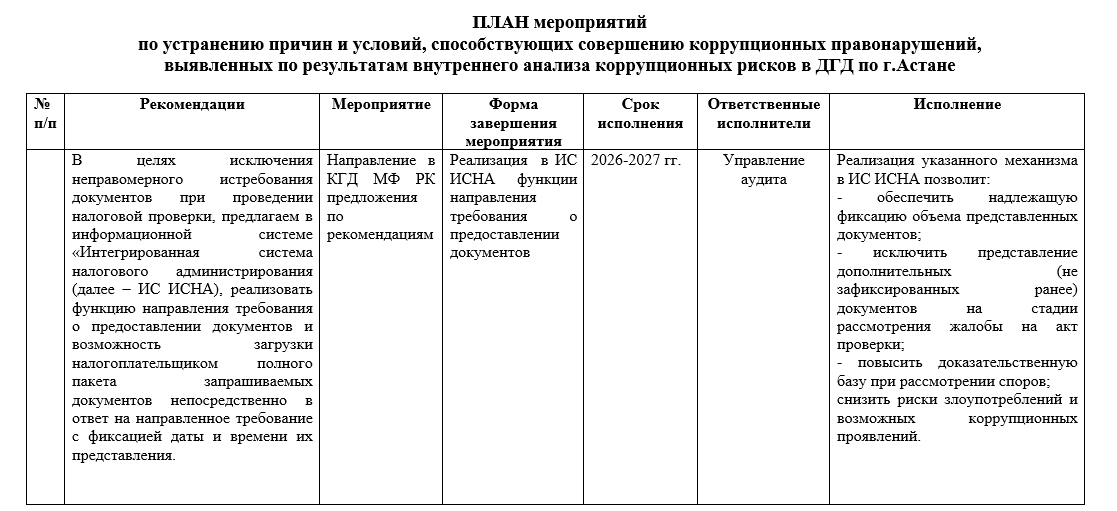

The legality and completeness of requesting documents during a tax audit.

Description of corruption risk

When conducting tax audits, the requirement of the state revenue authorities to provide the necessary documents is mainly primary accounting documents, balance sheets, account cards, contracts, acts of completed works and other documents. At the same time, the volume of such documents is a significant number of pages that the taxpayer needs to scan in order to embed them in the information system. However, the technical limitation regarding the loading and storage of the data array has not been determined. Currently, the direction of the request for the provision of documents is implemented in the information system in the taxpayer's office. It is proposed in the information system "Integrated Tax Administration System (hereinafter referred to as IS ISNA), the implementation of this mechanism will allow: to ensure proper recording of the volume of submitted documents; to exclude the submission of additional (not previously recorded) documents at the stage of consideration of a complaint against an inspection report; to increase the evidentiary base when considering disputes; reduce the risks of abuse and possible corruption.

Recommendations for risk management

The implementation in the ISNA IP of the function of sending a request for documents and the possibility for the taxpayer to download the full package of requested documents directly in response to the request, with the date and time of their submission recorded.

Source : https://www.gov.kz/memleket/entities/kgd-astana/press/news/details/1235565?lang=ru